The number of building permits issued for single-family homes is the best indicator of how many newly built homes will begin to come to market over the next few months. According to the latest U.S. Census Bureau and U.S. Department of Housing & Urban Development Residential Construction Report, the number of building permits issued in January was 1,551,000. This is a 9.2% increase from December.

How will this impact buyers?

New inventory means more options. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR),explained how this is good news for the housing market – especially for those looking to buy:

“More construction will mean more housing inventory for consumers in the later months of this year…Spring months could still be quite tough for buyers since it takes time to convert housing starts into actual housing completions.”

How will this impact sellers?

More inventory means more competition. Yun continues to say:

“As trade-up buyers move into these newly completed homes in the near future, their existing homes will be released onto the market.”

Today, because of the tremendous lack of inventory, a seller can potentially anticipate:

A great sale price on their house as buyers engage in potential bidding wars.

A quick sale as buyers have little inventory to choose from.

Fewer hassles as buyers want to smoothly secure a contract.

Bottom Line

If you’re considering selling your house, you’ll want to list sooner rather than later. This way, you’ll get ahead of this new competition coming to market and ensure the most attention toward your listing and the best price for your house.

Mortgage rates are sitting near record lows — and that’s spurring a wave of refinancing activity as Americans look to take advantage of the savings a cheaper interest rate could bring.

Refinance loan volume jumped to the highest level since June 2013 in early February, especially among jumbo mortgage borrowers, on the heels of lower mortgage rates, according to data from the Mortgage Bankers Association. The average interest rate for a 30-year fixed-rate mortgage fell to 3.45% two weeks ago, Freddie Mac FMCC, -0.52% reported, the lowest level since October 2016. Since then, it has risen slightly to 3.47%.

More than 11 million homeowners stand save to an average of $268 per month on their mortgages if they were to refinance at current rates, real-estate data firm Black Knight reported last week.

“Almost anybody should be checking if there’s an opportunity to refinance,” said Tendayi Kapfidze, chief economist at LendingTree TREE, +3.57%. “It doesn’t cost anything to talk to a lender and see what rate they might get you in this marketplace.”

But refinancing isn’t foolproof. Taking out a new home loan can cost you thousands of dollars in fees. And making the wrong choices can significantly reduce your potential savings. Here are five questions homeowners should ask themselves before taking the plunge with a mortgage refinance.

How long will I stay in this home?

Mortgages are paid out over the span of many years, and during the initial period most of your payments will go toward the interest rather than the principal owed on the loan.

As a result, time is one of the most significant factors in determining whether a refinance makes financial sense. “You want to keep the loan long enough for the monthly savings to exceed the closing costs — that varies a lot depending on the fees,” said Holden Lewis, mortgage expert at personal-finance website NerdWallet.

Homeowners who are planning to move to a new house in the next five or so years may actually save more by sticking with their existing mortgage rather than refinancing, given the fees you have to pay the lender.

‘You want to keep the loan long enough for the monthly savings to exceed the closing costs.’—Holden Lewis, mortgage expert at NerdWallet

On the flipside, people who are in their forever homes could benefit from taking out a 15-year loan rather than a 30-year loan, Lewis said. The average interest rate on the 15-year fixed-rate mortgage is typically lower than the 30-year loan — it currently stands at 2.97%. So while these loans require larger monthly payments, the aggregate savings are greater.

A 15-year loan also would allow the homeowner to build equity faster, which they could then tap through a home-equity loan further down the road if unexpected expenses arise.

How much will I save?

To save money with a refinance, the general rule of thumb is that the new interest rate needs to be 50 basis points lower than your current one, Kapfidze said. But when looking at the average rates reported by Freddie Mac, it’s important to remember that the rates offered by lenders can be even better.

“Because typically a lot of the rates you see are average rates, it means that half the rates are below that,” Kapfidze said.

To save money with a refinance, the new interest rate should be 50 basis points lower than your current one.

Comparison shopping, as a result, is critical in order to score the best deal. Lenders don’t just compete on interest rates. They also can adjust how much you spend in closing costs. Another factor that can shift overall savings is the discount points — these are fees lenders collect at closing in order to reduce the long-term interest rate. If you can pay more at closing, this could bring your interest rate down even further.

Am I paying mortgage insurance?

There are two instances when borrowers must pay mortgage insurance: If they get a Federal Housing Administration (FHA) loan, or if they get a conventional loan with a down payments of less than 20%.

When refinancing, it’s critical to review what type of loan you can get and how much equity you have. “Refinancing when you’re going to have 20% equity or more is going to give you the best deal because you’re not going to have mortgage insurance,” Lewis said.

Getting rid of mortgage insurance will boost your overall savings and can make a refinance worth it even if you’re outside the 50-basis-point threshold.

If you haven’t built much equity in your home through your monthly mortgage payments, but have a chunk of cash in savings, a cash-in refinance can help push you above the 20% mark, Kapfidze said, adding that this could be a decent use of your tax dollars.

‘Your better credit score will put you into a better rate.’—Tendayi Kapfidze, chief economist at LendingTree

Is my financial house in order?

A recent study from LendingTree found that one in four mortgage refinance applications is denied. The most common reason applications are denied is that the borrower’s debt-to-income ratio is too high, followed by having poor credit.

Taking steps to improve both your debt-to-income ratio and your credit score ahead of applying for a new home loan will increase the odds of getting improved. “If there’s anything you can do to reduce your non-mortgage debts, that’s going to help,” Kapfdize said. It’s also important to verify that there are no errors on your credit report.

Another reason to review your credit history: Your score has likely improved as you’ve been paying off your mortgage. “Your better credit score will put you into a better rate,” Kapfidze said.

When pursuing a refinance, don’t forget about your existing lender. “If they know you’re shopping around, they should be motivated to give you the best deal,” said Rick Sharga, a mortgage industry veteran and consultant.

Because your existing lender already has your personal information and payment history, refinancing with them can often be an easier process. Additionally, they have a vested interest in keeping your business, which will push them to compete as much as possible with other lenders’ offers.

Another way refinancing with your existing lender can mean better savings is by amortizing the new loan. Your lender will have a sense of how long you’ve had your existing loan for, and as a borrower you will save more by refinancing to a shorter duration than getting a new 30- or 15-year loan and starting from square one.

This story was originally published on Feb. 10, 2020 and has been updated.

Beautiful white daffodil flowers in morning sunlight, taken in the springtime.

Spring is right around the corner, so flowers are starting to bloom, and many potential homebuyers are getting ready to step into the market. If you’re thinking of buying this season, here’s how mortgage interest rates are working in your favor.

“If you’re in the market to buy a home, today’s average mortgage rates are something to celebrate compared to almost any year since 1971…

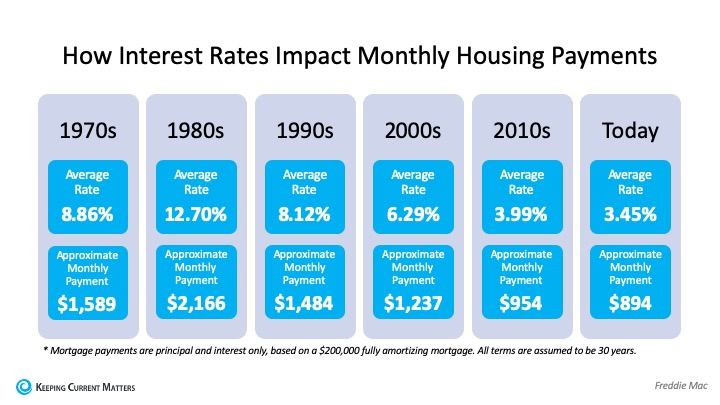

Mortgage rates change frequently. Over the last 45 years, they have ranged from a high of 18.63% (1981) to a low of 3.31% (2012). While it’s not likely that the average 30-year fixed mortgage rate will return to its record low, the current average rate of 3.45% is pretty close — all to your advantage.”

To put this in perspective, the following chart from the same article shows how average mortgage rates by decade have impacted the approximate monthly payment of a $200,000 home over time:Clearly, when rates are low – like they are today – qualified buyers can benefit significantly over time.

Keep in mind, if interest rates go up, this can push many potential homebuyers out of the market. The National Association of Home Builders (NAHB) notes:

“Prospective home buyers are also adversely affected when interest rates rise. NAHB’s priced-out estimates show that, depending on the starting rate, a quarter-point increase in the rate of 3.75% on a 30-year fixed rate mortgage can price over 1.3 million U.S. households out of the market for the median-priced new home.”

Bottom Line

You certainly don’t want to be priced out of the market this year, and waiting may mean a significant change in your potential mortgage payment should rates start to rise. If your financial situation allows, now may be a great time to lock in at a low mortgage rate to benefit greatly over the lifetime of your loan.

Suggested caption/status: This week, the 30-year fixed-rate mortgage averaged 3.45%! Message me and we can review what you can afford in today’s market.